Introduction

The term “heatwave” was introduced into the oceanographic literature in 2013 to describe unexpected warm events in 2011 off of western Australia (Pearce and Feng, 2013) and in 2012 in the Northwest Atlantic (Mills et al., 2013). These events prompted an international effort to define marine heatwaves and to understand their statistical properties (Hobday et al., 2016a; Scannell et al., 2016; Oliver et al., 2018). While these events reveal interesting atmosphere-ocean interactions, they are perhaps most notable for what they reveal about how humans interact with ocean ecosystems. One of the side effects of extreme events is that they can motivate actions to prevent adverse consequences in the future. For example, Hurricane Katrina and Superstorm Sandy prompted communities in the affected regions to start planning for future storms (Ford et al., 2011; Brown et al., 2014). Upwelling of corrosive waters along the coasts of Oregon and Washington motivated the development of technology to monitor carbonate chemistry and manage water in shellfish hatcheries (Barton et al., 2015). In this paper, we consider the consequences of warming trends and events in the Gulf of Maine. In particular, we will explore whether lessons from the 2012 heatwave spurred adaptive human actions that mitigated similar impacts during a subsequent heatwave in 2016.

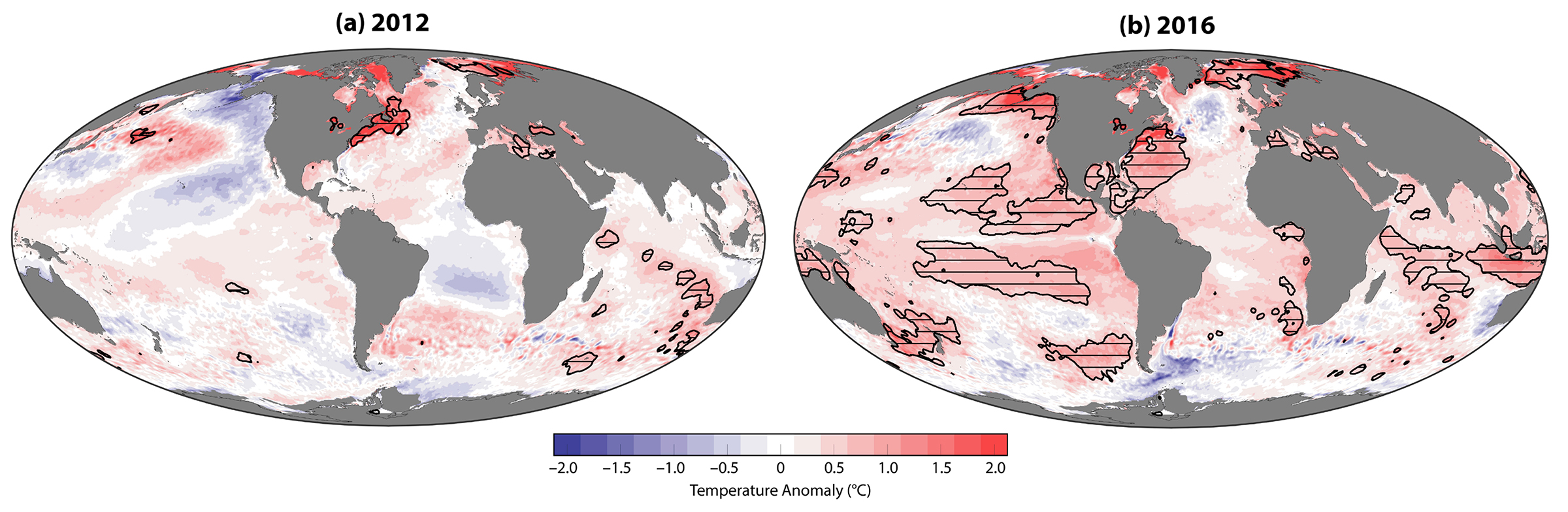

In 2012, temperatures were above average across much of the North Atlantic (Figure 1a), and the temperature anomaly from Cape Hatteras to the Grand Banks was more than 2°C above the 1982–2011 average.1 Hobday et al. (2016a) define a marine heatwave as a region with temperatures above the 90th percentile of the day-specific climatology for more than five days. At the annual scale, we mapped the number of days in a year with temperatures above the 90th percentile of the 30-year climatology. We then say that a location experienced a significant heatwave if more than 100 days (not necessarily consecutive) were above the threshold during the year. The 2012 event in the Northwest Atlantic region easily meets this criterion, and similar events also occurred in 2012 in the Barents and Kara Seas, the Mediterranean and Black Seas, and off the coast of western Australia (Figure 1a, regions outlined in blue).

Figure 1. Annual average sea surface temperature anomalies in (a) 2012 and (b) 2016. Anomalies are relative to the 1982–2011 climatology. Potential heatwaves are highlighted. These regions had more than 100 days in the year above the 90th percentile. > High res figure

|

The Northwest Atlantic event was most intense and persistent in the Gulf of Maine. An influx of warm water at depth in 2011 set the background for the event (Townsend et al., 2015). An anomalously warm autumn and winter led to reduced cooling and allowed the Gulf of Maine to retain considerable heat into the spring (Chen et al., 2014). Finally, very warm weather during the spring and summer throughout the western Atlantic expanded the spatial extent of the event (Peterson et al., 2013).

The 2012 heatwave was also notable for its impact on the ecosystem and the fisheries of the region. As we described in our previous Oceanography paper (Mills et al., 2013), the heatwave brought mid-Atlantic species such as longfin squid and blue crabs into the Gulf of Maine. It also contributed to low recruitment in Gulf of Maine cod (Pershing et al., 2015). However, the largest economic impact was observed in the region’s highly valuable lobster fishery.

Maine accounts for 83% of US lobster landings and had a landed value of $540M2 in 2016. The lobster fishery in Maine is the primary source of income for many coastal communities (Steneck et al., 2011). The fishery operates year-round, but landings are highly seasonal and dominated by very high catch rates of newly molted lobsters during the summer and autumn (Holland, 2011). In 2012, lobstermen3 reported catching newly molted lobsters in April, rather than the typical timing in July. At the statewide level, landing rates suddenly increased in early June, nearly a month ahead of the typical period (Mills et al., 2013, 2017). The sudden influx of lobsters created a glut of product that could not be processed and cleared through the supply chain, resulting in a rapid drop in the price lobstermen received for their catches. Exacerbating the supply chain bottleneck was the fact that the Canadian lobster fishery also had unusually high spring landings; the joint impact was low prices on both sides of the border accompanied by Canadian protests and blockades of lobster imports coming from Maine. Even though lobstermen in Maine landed over 20% more lobster than in the previous year, a record at the time, the value of the fishery only increased 2% due to the depressed prices4.

The 2012 event prompted a series of changes in the Maine lobster fishery to avoid a similar price collapse in the future. In 2013, lobstermen voted to support a generic advertising campaign through a surcharge levied on their annual licensing fee (Idlebrook, 2013). The resulting Maine Lobster Marketing Collaborative focused on promoting “newshell” lobsters—lobsters with softer shells that are common during the summer and constitute the bulk of the catch—in domestic restaurant centers of the eastern seaboard. The collaborative also focused on educating chefs, garnering media impressions, and linking Maine’s lobster dealers directly to retail buyers in urban markets through an enhanced website communications platform. At the same time, the capacity to store and process lobsters in the state increased, with new facilities being built in several places, including Hancock, Portland, Prospect Harbor, Saco, and Scarborough (Associated Press, 2013; Van Allen, 2014).

Finally, we were asked informally by Maine’s Department of Marine Resources and by individual lobstermen to investigate whether the fishery’s early and sudden shift into the summer mode could have been predicted. We found a robust, linear relationship between the date when statewide landings begin to increase (typically around July 1) and water temperatures in March and April (Mills et al., 2017). We built this into an operational forecast system that uses the subsurface temperatures available from the Northeast Regional Association of Coastal Ocean Observing Systems (NERACOOS; Pettigrew et al., 2011). In 2015 and again in 2016, we announced our initial forecast at the Maine Fishermen’s Forum, an annual conference and trade show that occurs the first weekend in March. We revised the forecast each week from early March through mid-April and posted the weekly update on our website, along with a more in-depth description of current ocean conditions and their impacts on the forecast.

In 2016, the time series of daily temperatures was nearly identical to conditions in 2012. This provides an opportunity to study whether and how the coupled natural and human system that is the Maine lobster fishery has adapted to temperature changes.

1 We use NOAA’s optimum interpolation sea surface temperature (OISST) product (Reynolds et al., 2007; downloaded from https://www.ncei.noaa.gov/thredds/blended-global/oisst-catalog.html) throughout this article. We produced daily climatologies for the period 1982–2011, including mean and standard deviation. All anomalies are reported relative to this period.

2 https://www.st.nmfs.noaa.gov/commercial-fisheries/commercial-landings/annual-landings/index

3 Lobster harvesters in Maine are overwhelmingly male, but the number of women participating in the fishery is increasing. Based on our conversations with some of the leading female captains, there is overwhelming support for the term “lobsterman” rather than something gender neutral such as “lobster fisher.”

4 Lobster landings and lobster price data were downloaded from Maine’s Department of Marine Resources (http://www.maine.gov/dmr/commercial-fishing/landings/index.html). Annual average landings are available from 1928 to 2016. Monthly average landings and price are available since 2004.

Ocean Temperatures in 2016

Elevated carbon dioxide levels and a very strong El Niño combined to make global average surface temperatures in 2016 the highest in the instrumental record to date (Dunn et al., 2017). Compared with 2012, many large ocean regions exceeded the 90th percentile threshold for more than 100 days in 2016. These regions included the Gulf of Alaska, the waters between Australia and New Zealand, the Norwegian and Barents Seas, the Mediterranean Sea, the Gulf of Mexico, the Caribbean Sea, and a large region extending from the Caribbean to the Gulf of Maine and the Scotian Shelf (Figure 1b). The most widely reported biological impact in 2016 was a global mass coral-bleaching event (Hughes et al., 2018).

Temperatures in the Gulf of Maine (defined as 40.375°–45.125°N and 70.875°–65.375°W) were very warm at the start of the 2016, exceeding the record conditions set in 2012 (Figure 2a). Conditions were consistently above the 90th percentile threshold through mid-April (Figure 2b). Though still well above average, the temperatures for most of the spring and early summer period fell below the 90th percentile criterion. In contrast, summer temperatures in 2012 were consistently above the heatwave criterion, and daily records were set throughout the summer. In early September 2016, temperatures rose rapidly and reached their maximum for the year—nearly a month later than normal. Temperatures remained above the 90th percentile level through late November. Overall, 2016 registered as the second warmest year for the Gulf of Maine in the OISST record and was less than 0.5°C below the 2012 level.

Figure 2. (a) Gulf of Maine temperature cycle in 2012 (red) and 2016 (black) relative to the mean and range (two standard deviation gray region). (b) 2012 (red) and 2016 (black) temperature anomalies. Heavy lines indicate periods above the 90th percentile. Circles denote record temperatures (1982–2016). > High res figure

|

Temperature Impacts on Maine’s Lobster Fishery

The 2012 marine heatwave had a profound impact on Maine’s lobster fishery (Mills et al., 2013). During the winter of 2016, early indicators suggested the Gulf of Maine was facing temperature conditions similar to those of 2012. On March 4, we issued a forecast that lobster landings would begin to increase rapidly in early June, instead of the more typical July increase (Mills et al., 2017). We continued to update the forecast every week until mid-April. Our final forecast was for the statewide landing rate to begin increasing on June 17, with a 97% chance of a very to extremely early year.

We received two surprises in 2016. First, despite demonstrated accuracy, our forecast was viewed as an unwelcome disruption. As in the prior year, we announced our forecast at the Maine Fishermen’s Forum, an important event attended by lobstermen, industry leaders, and managers. In an unusual coincidence of scheduling, the 2016 Forum occurred the same weekend as the Boston Seafood Expo, a major annual event for the global seafood industry, where many deals for seafood products, including American lobster, are negotiated. We heard from lobster dealers that our forecast of an early start to the high-landings period for Maine’s lobster fishery caused their customers to assume a high volume of landings was imminent (our forecast only considered timing, not volume). They reported receiving lower prices for their products than they expected. Many lobstermen also became jaded with the forecast during 2016, particularly as high levels of media coverage kept the forecast in the news, with most stories implying that the 2016 fishing season would prove to be a repeat of the 2012 season (Murphy, 2016). Lobstermen subsequently reported that the early influx of newly molted lobsters that occurred in 2012 did not repeat in 2016, perhaps because of the less-extreme temperatures during the spring and early summer (Figure 2). It looked like our forecast had failed and that it had created unintended consequences for the industry. Based on this feedback, we decided not to issue a public forecast in 2017 (Associated Press, 2017).

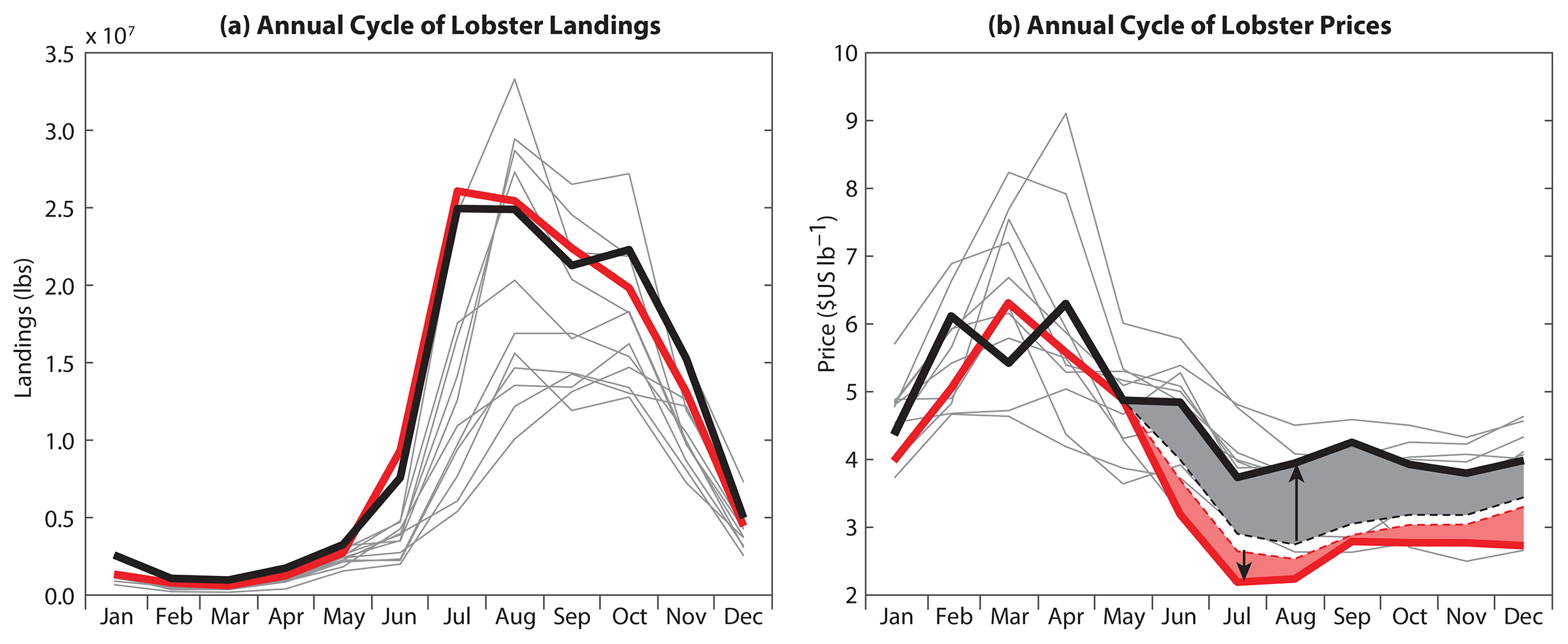

Our second surprise occurred in 2017 when the 2016 lobster landings and price data were released. The annual cycle of landings for 2016 was nearly identical to the 2012 pattern (Figure 3a), and the switch to the high landings period occurred on June 14, four days earlier than our forecast (Mills et al., 2017). However, the annual cycle of the prices paid to lobstermen for their catches was very different. Rather than declining abruptly as landing rates increased in June and July, prices declined gradually and remained stable throughout the summer (Figure 3b).

Figure 3. Annual cycles of lobster landings (a) and lobster prices (b) in the Maine fishery. The two heatwave years of 2012 (red) and 2016 (black) are emphasized relative to the 2004–2016 record (gray lines). The shaded regions in (b) show the difference between observed prices (solid lines) and expected prices calculated from linear models that relate price in one month to the price in the prior month and the current month’s landings. Models were initialized in May and forced with observed landings. The monthly modeled prices had an average standard deviation of $0.61 and $0.43 in 2012 and 2016, respectively. > High res figure

|

One of the challenges with interpreting time series of commodity prices is knowing what price would be reasonably expected given the current conditions. We fit simple linear models relating the lobster price (Pj(t)) in month j and year t to the prior month’s price:

The parameters for each of the monthly models were fit using linear regression. Except for March, the models were all significant (p<0.05, R2 ranged from 0.40 to 0.93), indicating a high degree of autocorrelation in lobster prices. This term captures some of the current market conditions, which include global demand for lobster and the supply of lobster from the United States and Canada.

We then considered whether landings have an impact on prices. We added landings within the month (Qj(t)) to (1),

and refit the models using linear regression. Adding the landings term improved the models (as indicated by a lower AIC score for model 2) for May, June, July, and September.

The monthly models encapsulate the expected relationships between prices and landings. We used the monthly price models in a Monte Carlo procedure to recreate potential price histories for 2012 and 2016 using the observed landings in those years. For each month between June and December we fit 14 different models by excluding the data from one year. Based on the AIC score, we selected either the autoregressive model (1) or the model with landings (2). Note that the different models for a month did not necessarily have the same forms, though none of the months had more than two models with different forms. We then randomly selected one of the June models and used it to calculate the distribution of June prices given May prices and June landings. We selected a value from this distribution and applied it to a randomly selected July price model. The estimated July price was then used as input to an August model, and the process continued for the rest of the year. We repeated the process 5,000 times.

The linear models suggest that a decline in prices between May and June should have occurred in both years, with 2012 expected to have a larger decline due to the slightly higher volume of lobsters landed in June of that year (Figure 3b, dashed lines). Based on May prices and the landings the rest of the year, the prices in 2012 and 2016 should have been similar. Instead, the prices in 2012 were slightly lower than expected prices (red line) while those in 2016 were considerably higher than expected (black line). Multiplying the difference between the actual and modeled prices (shaded regions) by the landings time series suggests that the anomalous behavior in 2012 resulted in a $38M reduction in the total landed value of the fishery (95% confidence interval: −$117M to $28M). In 2016, the anomalously high prices led to an extra $108M in added value (95% confidence interval: $54M to $158M).

What happened in 2016 to allow Maine’s lobster fishery to achieve a record value despite 2012-like conditions? Our linear models suggest that the prices lobstermen receive for their catches is inversely related to the volume of landings during the summer and autumn. This implies a classic supply and demand relationship, with more supply (more landings) leading to a decline in price. The difference between 2016 and 2012 suggests a possible increase in demand for lobster over the intervening period and a reduction of the processing bottleneck that led to the price shock in 2012 (Mills et al., 2013).

The significant post-2012 investments made in processing capacity to handle higher volumes of “newshell” lobster likely reduced the potential of a supply bottleneck and price crash. This processing expansion has been accompanied by growth in domestic and international markets for processed and live lobster, leading to a more diversified supply chain that, in theory, may increase resilience to climate shocks like marine heatwaves (Lim-Camacho et al., 2017). The 2016 experience suggests that these factors have combined to create more favorable market conditions for the lobster industry. While we would love to say that our forecast played a role in the high prices observed in summer 2016, we are not able to do more than speculate. It is possible that the forecast prompted dealers to sell off more of their inventory of stored lobster in anticipation of higher landings and to make up for the lower prices they reported being offered by their customers. The high prices paid to lobstermen during the summer would reflect increased overall demand, including the need for dealers to rebuild their inventories. If this were the case, the impact of the forecast on prices would imply an over-reaction to the forecast, one that benefited lobstermen but hurt lobster dealers, at least in the short term. It is important to keep in mind that no two years are exactly alike. Although 2012 and 2016 were similar in many ways, it is possible that the complex system of lobsters, lobstermen, dealers, and markets has thresholds that were exceeded only in 2012, potentially contributing to the difference in the price response between the two years.

Further Reflections on 2012 and 2016

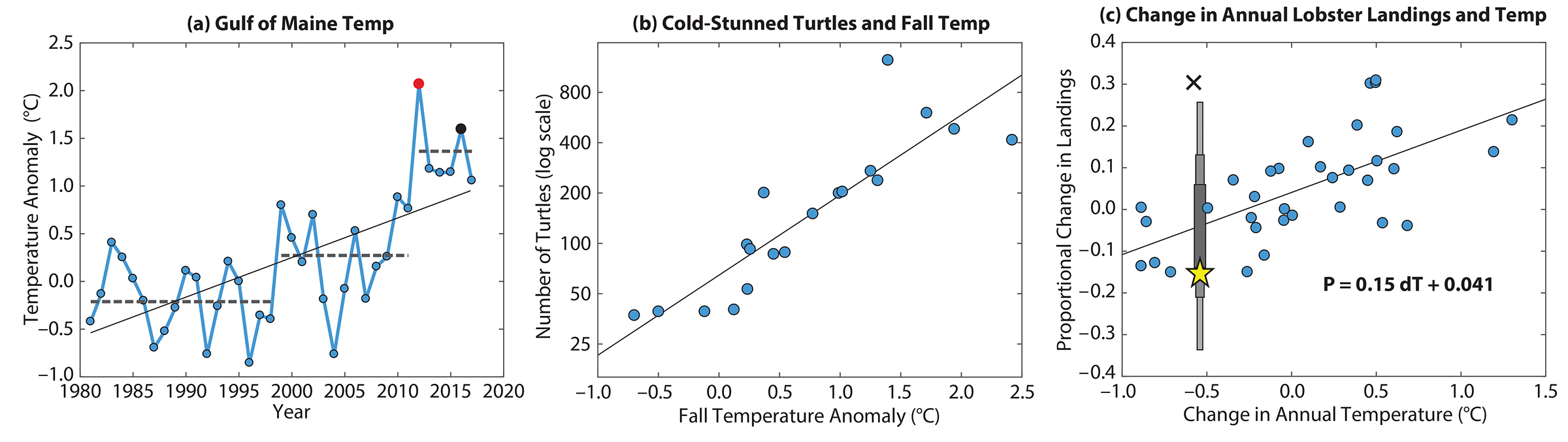

The acute heatwaves of 2012 and 2016 are part of a broader pattern of rapid change within the Gulf of Maine ecosystem. Between 1982 and 2017, the region has warmed at a rate of 0.04°C yr–1 or more than four times the global average rate over this period (Figure 4a). While there is a significant warming trend, the warming has not been steady. We used a chronological clustering algorithm (Legendre et al., 1985) to identify breakpoints that divide the temperature data into contiguous pieces where the values within each piece are more similar to each other than they are to values in adjacent pieces. This algorithm identified three periods: 1981–1998, 1999–2011, and 2012–2017. Prior to 1999, the mean temperature of the Gulf of Maine was −0.21° below the 1982–2011 average. The temperature in 1999 was the warmest in the satellite record up to that time and was 1.2° higher than in the previous year. The next 13 years were highly variable. High temperatures comparable to 1999 occurred in 2002, 2006, 2009, and 2010. However, several years were cooler than average—notably, 2004 was the second coldest year since 1981. The 2012 heatwave started a period of very high temperatures, and the 2012–2017 mean was 1.4° above average.

Figure 4. (a) Annual mean temperature anomalies from the Gulf of Maine. The trend line has a slope of 0.042°yr–1 (R2 = 0.43, p<0.01). The horizontal dashed lines are the mean temperatures over three periods selected using chronological clustering. (b) Number of cold-stunned turtles in Massachusetts Bay (log-transformed) as a function of the fall (4th quarter) temperature anomaly (R2 = 0.77, p<0.001). Both data have significant trends over 1999–2017. When the trends are removed, the relationship is still highly significant (R2 = 0.64, p<0.001). (c) Proportional change (Q(t+1) = (L(t+1) – L(t))/L(t)) in Maine lobster landings modeled as a function of the change in the annual mean temperature (R2 = 0.43, p<0.01; 2004, indicated by an “x” is an outlier and was excluded from the regression). The model suggests a 5% decline in landings for 2017 while the fishery experienced a 15% decline (yellow star). The 50%, 75%, and 95% prediction intervals are indicated by the gray boxes. > High res figure

|

In addition to the annual changes, the seasonality of the Gulf of Maine is also changing. Thomas et al. (2017) found that the recent warming has been strongest in the summer and autumn, continuing a pattern reported earlier (Friedland and Hare, 2007). This signature is readily apparent in the 2012 and 2016 temperature cycles (Figure 2a). If summer is defined as the period when temperatures are within 0.5°C of the climatological summer maximum, summer-like conditions are extending by 1–2 days yr–1 in the Gulf of Maine, with stronger expansion during autumn than spring (Thomas et al., 2017).

The shift in seasonality is causing changes in the distribution and abundance of fish in the region. Henderson et al. (2017) found that changes in the center of fish and invertebrate biomass on the Northwest Atlantic shelf were more strongly linked to lengthening summers than to changes in the spring phenology. The fact that autumn is warming faster than winter means that, on average, the drop in temperature between autumn and winter is increasing. This has a potentially serious effect on species that migrate in and out of the Gulf of Maine. For example, warm waters in the summer and autumn are making the Gulf of Maine more favorable for sea turtles. Turtles that have not returned south when colder water temperatures prevail can be “cold-stunned” or even killed. The log-transformed numbers of cold-stunned turtles5 recorded from the 1998/1999 through the 2017/2018 seasons are strongly correlated with autumn temperatures (Figure 4b, R2 = 0.77, p<0.001). Both turtle encounters and autumn temperatures have significant trends, and the presence of trends raises the possibility that the increase in cold-stunned turtles could be due to an increase in the number of turtles. When the trends are removed from both time series, the relationship is still highly significant (R2 = 0.64, p<0.001). This suggests that the exceptional numbers of cold-stunned turtles in recent years are related to increasing numbers of turtles north of Cape Cod and to the warmer autumn conditions.

Large changes in temperature at the annual scale also have the potential to impact animal populations. This last year (2017) was cooler than 2016, especially in the spring and summer. When a cool year follows a warm year, lobster landings in Maine tend to decrease, and there is a strong linear relationship between the percentage change in landings from one year to the next and the change in the annual Gulf of Maine temperature anomaly (Figure 4c, R2 = 0.43, p<0.01). Note that 2004 was an outlier and was excluded from the regression; however, the relationship is still significant (R2 = 0.30, p<0.01) with 2004 included. The decline in landings when temperature declines may reflect reduced activity on the part of the lobsters, with colder temperatures making them less likely to wander into a trap, or fewer days on the water for lobstermen. It may also be a hangover from the previous year, with higher catch rates in a warm year reducing the available biomass in the following year. Based on the observed decline in annual temperatures between 2016 and 2017, we would expect a 4% decline in lobster landings. Instead, landings in 2017 were 15% lower than 2016 (Figure 4c). This is within the 75% prediction interval, but it is the largest percentage decline in landings since 1982. It is thus possible that we are seeing the beginning of the decline in the fishery predicted by several years of low lobster settlement (Oppenheim, 2016) and by a temperature-based population dynamic model (Le Bris et al., 2018).

Future of the Gulf of Maine

Since 2012, the Gulf of Maine has gained notoriety for its rapid pace of warming. This is part of a larger pattern of warming in the Northern Hemisphere that includes the Northwest Atlantic, the Barents Sea, and the Arctic (Figure 5a). The spatial pattern of warming in the North Atlantic has been interpreted as an indication of a slowdown in the Atlantic Meridional Overturning Circulation (AMOC; Rahmstorf et al., 2015; Caesar et al., 2018), a conclusion that is supported by experimental climate simulations using a very high-resolution climate model (Saba et al., 2016). The spatial pattern of warming in this simulation is strikingly similar to the pattern of warming observed in the last 15 years (Figure 5b) and may approach five times the global average. The warming in the Gulf of Maine in the model is driven by increased flow of warm bottom water into the Gulf of Maine associated with a slowdown in the AMOC (Saba et al., 2016). This mechanism is similar to the “Coupled Slope Water System” concept proposed by the MERCINA Working Group (2001) and to the recent observations of Townsend et al. (2015).

Figure 5. Sea surface warming rates from (a) observations over 1982–2016 and from (b) Saba et al.’s (2016) high-resolution climate projection. The colors indicate the percentile score of the warming rate at that pixel. Black regions have rates below 80%. Yellow regions have rates that exceed 99%. > High res figure

|

While it is likely that a significant decadal pattern is driving the recent acceleration of warming in the Northwest Atlantic (Pershing et al., 2015), it is also likely that this region will continue to warm at an above-average rate. This warming will have consequences for the ecosystem and for the human communities that depend on it. Long-term warming in this region has been linked to the collapse of the lobster fishery in southern New England and the explosion of the fishery in Maine and Canada (Le Bris et al., 2018). The future of these fisheries depends on the rate of warming. If the region warms as predicted by the ensemble of CMIP-5 global climate model simulations under the RCP 8.5 emissions scenario (~0.03°C yr–1), there may be some recovery in the southern New England lobster population, but it is unlikely to return to historical levels. If the higher rate of warming indicated by Saba et al. (2016) and by the trend in the last 35 years is realized, then the southern New England population will not be able to recover. The Le Bris et al. (2018) model indicates that the Gulf of Maine lobster population is currently very close to its maximum abundance. Continued warming will cause the population to decline, with the rate of decline proportional to the warming rate. While Maine’s lobster fishery may have adapted to the higher volumes, and especially the high volume of “newshell” lobster landed in 2012 and 2016, it is not clear how the industry will fare if landings decline as expected.

5 Data on the number of stranded or dead sea turtles on Cape Cod were provided through the Sea Turtle Stranding and Salvage Network from observations provided by Massachusetts Audubon Society’s Wellfleet Bay Wildlife Sanctuary. The database includes green (Chelonia mydas), Kemp’s ridley (Lepidochelys kempii), loggerhead (Caretta caretta), and hawksbill (Eretmochelys imbricata) turtles.

Adaptation Lessons

One of our goals for this paper is to add to the limited scientific literature that documents actual adaptation to climate change in marine social-ecological systems (Miller et al., 2018). The Northwest Atlantic heatwave of 2012 prompted Maine’s lobster industry to undertake a variety of autonomous (i.e., coping) and planned adaptation measures (sensu Moser and Ekstrom, 2010). The differential outcomes during another heatwave in 2016 indicate that these strategies helped buffer subsequent impacts to the industry, and lessons learned from adaptation between these two events may be useful to other fisheries beyond Maine.

In contrast with Lim-Camacho et al.’s (2015) finding that participants in Australian fisheries saw more opportunity for adaptation at the harvester level, adaptation between 2012 and 2016 in Maine’s lobster fishery occurred throughout the supply chain. At all levels of the industry, measures and strategies that were not available or used in 2012 may have buffered the impacts of the 2016 heatwave as harvesters, processors, and dealers all seem to have made adjustments in order to maximize the price of lobster as it moves up the value chain. These efforts were largely focused on markets and value, including efforts to keep lobsters cool and oxygenated onboard vessels and ashore, increased processing capacity, and the expansion of domestic and foreign markets.

Attention has been devoted to planning for climate-resilient fisheries on the part of management agencies (Busch et al., 2016); however, there is limited evidence of adaptation in the fishery management system following the 2012 heatwave experience. Failure to consider temperature influences on productivity of Gulf of Maine cod exacerbated the challenges of managing this stock (Pershing et al., 2015). Recruitment has also declined in yellowtail flounder in response to warming associated with a northward shift in the Gulf Stream (Xu et al., 2018). Both cod and yellowtail flounder once supported vibrant fisheries, but now the low quotas needed to rebuild their populations are constraining the ability of groundfish fishers to access more abundant stocks. Despite clear evidence that temperature is impacting these and other species, no fishery stock assessments in New England currently consider temperature. Thus, the quotas and fishery reference points (e.g., the biomass that produces maximum sustainable yield) reflect past conditions and the stock assessment process will not anticipate future change. This creates risk for the fish through quotas that may be too high and for the fisheries through rebuilding targets and timelines that are unrealistic (Pershing et al., 2015).

In addition to adaptation within the industry, management measures adopted in Maine’s lobster fishery have enhanced population resilience. The collapse of lobster in southern New England and the increase in Maine is more than just the population tracking climate velocity (e.g., Pinsky et al., 2013). Practices developed by Maine lobstermen to protect large lobsters and reproductive females allowed this region to capitalize on the near-optimum ecosystem conditions of the last decade, magnifying the difference between the two stocks (Le Bris et al., 2018). Maintaining these practices is projected to allow the fishery to decline at a manageable rate over the next 30 years to levels comparable to those prior to the recent lobster boom (Le Bris et al., 2018). Such approaches to reduce non-climate stress on populations will be important adaptation strategies in other fisheries as well (Pinsky and Mantua, 2014). In contrast, decades of cod overfishing in the Gulf of Maine resulted in a significant truncation of the population’s age structure as well as a decline in biomass, which likely made this stock much more sensitive to environmental changes (e.g., Ottersen et al., 2013; Le Bris et al., 2015; Barneche et al., 2018).

The recent heatwaves in the Gulf of Maine demonstrate that unexpected events can lead to adaptive change. As climate change progresses, marine ecosystem conditions will increasingly exceed past experience (Henson et al., 2017; Frölicher and Laufkötter, 2018). This will mean that the cycle we observed in Maine lobster of shock followed by adjustment will need to occur more frequently. There is a growing interest in developing operational ocean forecasts at a range of temporal scales (Hobday et al., 2016b; Payne et al., 2017; Tommasi et al., 2017). These forecasts could provide the basis for long-range planning, allowing individuals, companies, and management bodies to minimize costs associated with the shock-phase of the adaptation cycle. Our experience with developing forecasts for the Maine lobster fishery indicates that there will be considerable challenges in getting stakeholders to incorporate these products into their planning and potentially unintended consequences for different stakeholder groups. While increasing accuracy of weather forecasts is often cited as a main reason for their increased use as a basis for decision-making, it is also noteworthy that we have daily experience with these products. This experience allows us to build trust in the products and to gain a more intuitive understanding of what, for example, a 75% chance of rain means. Co-development of forecasts with potential users may increase the likelihood that forecasts are used (Hobday et al., 2016b); however, in contrast with weather forecasts, users of annual or decadal forecast products will not have the opportunity to gain an understanding of the forecasts through regular experience. Applying long-range forecasts in marine industries, and more generally throughout society, will require shifts in mindsets of both producers and consumers of forecast products.